Sunday, December 25, 2011

Holiday Break -- See you after the new year

Sunday, December 18, 2011

The incompetent and unscrupulous: Confidence in the age of MF Global

That is reserved for the unscrupulous. The unscrupulous are sometimes incompetent. But often they are quite competent at taking our money under false pretenses.

What the recent MF Global bankruptcy--the eighth largest in U.S. history--tells us is that the world's financial system may be moving headlong into a collision of incompetence with unscrupulousness. (Full disclosure: I had a small account with MF Global and so have had a ringside seat, so to speak, in the bankruptcy proceedings.) I do not mean to say that before now there was no unscrupulous behavior in the financial system. What I mean to say is that it does not matter how competent someone believes a firm is at investing or handling money; if the firm is perceived as dishonest, that's it!

So far the revival of stock and commodity markets around the globe via enormously stimulative budget and monetary policy has assured most people with invested money that the authorities are, in fact, competent to manage downturns, even severe ones. Markets may not be back to their previous highs, but they are a far cry from the devastation of late 2008 and early 2009.

Now the competence of those authorities is being questioned as Europe appears mired in a long battle to save the euro as the currency of its 17-country Eurozone. The question is: Should the average investor--the buy-and-hold investor--stick it out once more and trust in the authorities to make things all better? That is a monumental question.

But soon that question will be competing with an even uglier one? Can I count on the institutions which hold my money and investments--primarily brokerages and banks--to deal honestly and fairly with me? Can I count of them not to steal my money?

As the questions of competence and trust converge, the financial system seems increasingly imperilled. If authorities do everything right, but investors believe they can no longer trust their brokers and banks not to steal their assets, the competence of the authorities in monetary and fiscal policy will simply not matter. And, if investors should simultaneously lose faith in the ability of authorities to handle the roiling financial crisis in Europe and lose trust in their brokers and banks to safeguard their money, we should be prepared for a wipeout that will make 2008 look like a day in the park.

This is the scenario lurking behind the MF Global collapse. Clearly, MF Global was incompetent at managing its risks including the risk that its lenders such as banks and hedge funds would withdraw funding for its positions. (Firms such as MF Global borrow money short-term to buy long-term assets and profit from the difference between the interest payments on short-term funding and the stream of revenues from long-term assets. The short-term funding must be periodically renewed. If this seems risky, it is.) The lenders stopped lending not necessarily because they believed MF Global to be unscrupulous, but because they believed the firm was no longer competent to manage the risks associated with its portfolio of highly leveraged investments. Fearing losses on their loans, they didn't roll over their financing.

Then came act two. MF Global misappropriated protected customer funds to support its precarious positions, especially those in European government bonds which seemed increasingly dicey this fall. Perhaps the firm felt it would be able to pay customers back once the fuss died down, and no one would be the wiser. But the fact that MF Global managers carefully covered their tracks in making the transfers tells us what we need to know. They believed what they were doing was illegal.

Here is the problem that regulators face. Prior to the MF Global collapse they had been able to say that no holder of a regulated futures account had ever suffered a loss of deposits (collateral or cash). Naturally, people lose money on futures positions every day. But that's a far cry from having money which has been deposited to support those positions simply stolen. That makes it impossible to collect money even if you win your bets, since the money that is supposed to be transferred to you from the people on the losing side of the trade just isn't there.

Futures accounts are not insured for such losses for the simple reason that the regulators wisely decreed that customer money and firm money have to be separated, and customer money simply cannot be used for the firm's own trading without customer consent. There was no consent, and there would have had to have been collateral posted or contractual obligations agreed to had there been any consent.

Worse still, the CME Group, owner of many U.S. futures exchanges, was the auditor for MF Global and thereby responsible for making sure customer money was properly segregated and actually in the right accounts every day. One would think that the owner of the exchanges would have a special interest in making sure one of the world's largest futures brokerages--with which the exchanges do business every day in huge volume--is handling customer money properly.

The result of the CME's poor supervision was a huge seize-up in futures trading as a significant portion of the world's largest players in the futures markets found their money frozen, waiting for someone to sort out the mess. Nearly six weeks after the collapse customers are only now getting a portion of their cash back, around two-thirds of it. The rest will have to wait for a claims process, and there is currently no guarantee that the remaining third will be paid back.

Now, if you are a futures trader and especially if you trade on behalf of clients, would you want to continue to trust the current U.S. regulatory system to safeguard your money? Why not go to say, Canada, where regulators appear to take their jobs more seriously and trade there? After all, Canadian customers of MF Global didn't lose a penny.

That's what the domestic futures exchanges and brokerage firms are facing. A gradual and perhaps persistent loss of business to someplace where traders feel assured about the safety of their funds. And, many small traders are simply giving up trading futures at all, believing the regulatory authorities are incompetent and the brokerages too crooked to deal with.

Now, I'm imagining such an outlook migrating to people holding stocks, bonds, and mutual funds at brokerages and mutual fund companies. I'm even imagining that outlook infecting regular checking and savings account holders at banks. It may already be happening in Europe in countries such as Italy and Greece where wealthy people seem to be shifting their money to safer banks in Germany or even outside of the Eurozone altogether.

These types of fears have a way of taking on a life of their own and spreading all of a sudden across the globe. I've mentioned before that Nicole Foss, writer for the financial commentary site The Automatic Earth, has said that liquidity and confidence are the same thing. If I lose confidence that my investments and cash in brokerage accounts and bank accounts are safe for whatever reason, then I will sell my holdings and withdraw my funds moving them to where I think they will be safe. If enough people do this, liquidity dries up as everyone heads for the exits at the same time. There are not nearly enough buyers to handle the sell orders in various markets. And, if people withdraw money from banks, the banks must quickly find some other source of liquidity than customer deposits. Such liquidity problems are already appearing at banks in Europe. And through it all, it will not matter whether investor fears are actually justified.

As the prosecutions of financial malfeasance rise, as the revelations of double dealing and outright theft abound, as the ability of European, American and Asian authorities to calm markets is eroded, the intersection of incompetence and unscrupulousness is poised to fling the global financial system into the dark unknown. These kinds of complete meltdowns have occurred in individual countries with disastrous results; Argentina comes to mind. But a grand failure of this sort on a global scale was only really hinted at in 2008. That's how bad it could be next time.

Sunday, December 11, 2011

Deconstructing "ethical oil"

You see, the site is a defense of the Canadian oil sands industry. The argument it makes is that because human rights standards are much better in Canada than in many other oil exporting nations, Canada should be considered a more "moral" source of oil. In fact, the oil from the oil sands is touted as a "fair trade choice."

Once I'd read through the site, it was hard to imagine why the oil sands industry would even want it online. If these people were working for me with the express mission of defending the oil sands, I would fire them. Let me explain why.

First, the site claims to be based on a book called Ethical Oil: The Case for Canada's Oil Sands. At the bottom of the EthicalOil.org home page the book is described as follows:

In Ethical Oil, Levant [the author] turns his attention to another hot-button topic: the ethical cost of our addiction to oil. While many North Americans may be aware of the financial and environmental price we pay for a gallon of gas or a barrel of oil, Levant argues that it is time we consider ethical factors as well.

I am certain you are now scratching your head thinking you could do a better job of arguing the case than that. Since when, I hear you saying, did things financial and environmental stop being moral issues? That's strike one.

But the embarrassment has only begun. A set of rotating stories under "Featured News" includes a photo of two burka-clad females in front of the White House holding a hand-lettered sign which says "Stop tar sands, Stop Canada, Americans4OPEC.com." This strange scene seems contrived, and it is. The accompanying text reads as follows:

Americans4OPEC: Blame Canada!

Earlier today, I snapped a few photos of Americans4OPEC, which today joined the anti-Keystone XL protests outside the White House. Here’s one of the photos and the group’s press statement. You can visit their website at Americans4OPEC.com

Americans4OPEC statement (sic), which is available on their website:

"For more than 40 years, we Americans have powered our businesses, fueled our cars, and made our lives more comfortable with the help of OPEC oil. We think that special relationship is worth protecting..."

This is the site's attempt at satire (and it's also intentionally misleading). After reading the story or clicking through to the Americans4OPEC site, if you haven't figured out that the burka-clad protesters aren't real and that this is a satire, a note in small type at the bottom (if you make it that far) will tell you that "Americans4OPEC is not a real organization, but a satire created by EthicalOil.org to highlight the choice Americans now have."

Okay, in order for a satire to work, you don't really want to tell the reader up front that what he or she is reading is a satire. You want the reader to figure this out; it's part of the fun. On the other hand, a satire, to be effective, really ought to be funny. This one isn't. Strike two!

Far more insidious is the confusion this site sows about the label "ethical." We might consider the mere purchase of certain products or services as unethical. Or we might consider the conditions under which a product is grown, mined, manufactured, or traded, or a service rendered as unethical.

For example, we might consider the purchase of African ivory as unethical. (It also happens to be illegal.) We might also consider it unethical to eat bluefin tuna--which is highly prized in raw fish dishes such as sushi--because the species has declined so much due to overfishing.

However, we don't say that the purchase of coffee is in and of itself unethical. We now sometimes say that the terms of trade for the coffee growers is often unfair and therefore unethical. And, this accounts for the growth of fair trade certified coffee. The feeling is that the grower ought to get more of the proceeds from his or her coffee than international trade arrangements and powerful food companies have provided in the past.

Obviously, the argument being made by EthicalOil.org is that Canadian oil from the oil sands is more ethical because of the conditions under which it is produced which exhibit higher concern for human rights than in many other exporting countries. And, now we see why the authors of the site do not wish to talk about environmental aspects of the oil sands. Because to do so would force us to include the first ethical category in our discussion: namely, whether it is moral for us to consume increasing amounts of oil or even any at all given the implications for pollution and climate change.

But let's accept for a moment that we should limit our discussion to the relative human rights records of various regimes which export oil. If we buy oil from Canada, or at least refined products made from oil produced in Canada, should we feel better about ourselves? Not particularly, would be my answer. The key fact about tradable oil is that it is fungible. It can be moved virtually anywhere in the world. If we don't buy oil from Saudi Arabia or any of the other regimes thought to be inimical to human rights, those regimes will simply sell their oil to someone else. None of it will go to waste.

The only way those regimes might be penalized is if total consumption worldwide slumped, driving prices down. But this would force us back onto the first ethical category: namely, that the most moral thing we could do is simply to consume a lot less oil. Naturally, the supporters of the site do not want to discuss this logical conclusion of their argument. (The site, however, unwittingly mentions conservation in one paragraph as a means to wean America off OPEC oil. So, the authors are unconsciously aware that reducing overall consumption is really the only way to reduce the perceived evils associated with oil use including that of rewarding oil-exporting regimes having poor human rights records.)

The argument for using less oil overall is simply rejected in the book upon which the site is based. Here's the conclusion to that book (available on Amazon for those who want to check it out without buying the book):

The world isn't throwing out the internal combustion engine anytime soon. In fact, in countries like India, China, and Brazil, the world is buying more cars than ever. So we're stuck with oil for a long time, whether we like it or not. The only question that remains is: if we have to produce oil, and we have to buy oil--and we absolutely must do both--whose oil should we do our best to support? Who can we trust to do it the most morally?

There can be no doubt: Canada does it best. We're an energy superpower. And we're an ethical superpower too, setting international standards for how we treat the environment and how we treat each other. And if our goal as moral citizens is to make the world a better place, then there is only one choice: to pump as much oil as we possibly can out of Fort McMurray. Pump and steam and dig and drill and get that oil out of the sand in any and every way we can. Every drop of oil from Alberta is one less drop from some fascist theocracy, or some brutal warlord; one less cent into the treasuries of Russia's secret police and al-Qaeda's murderers.

Canadian oil sands oil is the most ethical oil in the world, and the people who invest there, work there, and support the oil sands with their patronage and their encouragement should be proud. Whether they realize it or not, they are all, gradually, helping to make the world a more moral, humane, and better place.

Think about it. The action that will be the most moral is "to pump as much oil as we possibly can out of Fort McMurray." This is only moral if you limit your moral evaluation to the relative human rights records of oil exporters. Otherwise, it isn't. And, you must ignore the necessity of bringing down consumption worldwide to really force any pain on the aforementioned egregious exporters. This is hardly a compelling case. Strike three!

(There's actually a lot more to amuse you or befuddle you with its ineptitude on the EthicalOil.org site if you have the necessary inclination.)

While unlocking the oil in the oil sands is most certainly the carbon bomb for our atmosphere that its opponents say it is, to be fair, so is every other source of carbon fuel, including sources for supposedly "clean" natural gas. It is not so much that the Canadian oil sands are better or worse than other sources of fossil fuels, but rather that their exploitation is made inevitable by the way we live. If we don't like the oil sands, then we must build a society that does not require their exploitation. This is doable with the technology we have (but perhaps not with the politics we have). The originator of the "ethical oil" argument, however, tells us that it will be impossible to build such a society until very far into the future. He is wrong--dead wrong, I would say.

If this is the argument upon which "ethical oil" rests, then it is one of the most unethical arguments ever made. Believing such an argument or using it cynically to deceive others may condemn us to catastrophic and irreversible climate change. And, it will also prevent us from preparing for an orderly transition away from fossil fuels--a transition that may be forced upon us in the not-too-distant future.

Now how's that for ethics?

Sunday, December 04, 2011

Oryx and Crake comes to mosquito town

What may seem like a benefit to society isn't always a benefit except to those who profit from it. So much has been written about the evils of genetically engineered food crops that it would be redundant to rehearse them all here. But what if the offending genetic technology were to be trained on a human problem that everyone believes ought to be tackled, namely mosquito-borne diseases?

The idea is to create wingless mosquitoes that can't get off the ground and so die practically in the place of their birth. That idea is now a reality. And, where it has been tested, both in and out of the laboratory, it has been a smashing success, bringing mosquito populations down by 80 percent in very short order.

That means that diseases such as dengue fever, yellow fever and malaria which infect tens of millions of people each year would be considerably reduced.

But as with any alteration in an ecosystem, you can never do just one thing. What will the unintended consequences of such mass eradications be? The writer of the article cited above does acknowledge that mosquitoes are part of the food chain and their decline could affect birds and fish. He says that could have consequences for pollination since birds are part of this process for some plants. He also suggests such eradications might open a niche for an even nastier creature.

But then he goes on to say that "this could be one of the most human-friendly modifications we could make to our world. And it would certainly be no worse for the environment than our habit of clear-felling forest areas."

So, there you have it. Humans are creatures who routinely affect the surface of the Earth and the biosphere on a massive scale, so why not this modification which seems so small and so humane? I take my response from Dr. Phil of television fame: "So, how's that workin' out for you?"

This is the same logic that has been used to justify genetically engineered (GE) food crops, and then fiber crops such as cotton and trees, and finally crops that produce pharmaceuticals. Each introduction was always a step forward for human comfort and well-being. Now, we have weeds which resist the herbicide that only a decade ago was supposed to be the great savior of the cash crop farmer by reducing the chemical, labor and financial inputs of those who planted crops that resisted the same herbicide. That herbicide known as glyphosate may now be altering the microflora in the soil in a way that leads to so-called "sudden death" of GE crops.

We have butterflies that die from the pollen of corn. We have rising farmer suicide rates in India where GE cotton that was supposed to increase yields instead fell victim to disease leaving farmers destitute. And, we now have the specter of genetic contamination of food crops with genes from plants grown in the open to produce pharmaceuticals. Would you like a little insulin with your corn flakes?

I have no doubt that this new technique for controlling mosquito populations will spread. It seems as if it will be safer--for humans at least--than chemical sprays and more effective than bed nets. If this method of eradicating pests works well, where will we draw the line? Shall we rid ourselves of rats in cities? Seems like a good idea. How about loathsome raccoons who love our garbage and can carry rabies? Maybe you're feeling a little queasy about that one. Why not get rid of coyotes which destroy so much of our livestock each year? But wouldn't that upset the normal predator/prey balance for other species as well?

The effects of this type of mosquito eradication on local ecosystems may indeed be minor. But, there's really only one way to find out. Try it on a large scale in a lot of places. And, that's what scares me!

Sunday, November 27, 2011

Why isn't the Keystone pipeline extension going to eastern Canada?

___________________________________________________________________________________

RELATED UPDATE October 21, 2012: Canadians could free themselves from oil imports, but will they?

___________________________________________________________________________________Perhaps I should back up a bit for those who are scratching their heads because they know that Canada is a large oil exporter. Canada is indeed a large oil exporter. First, let's note that Canada's total petroleum production was 2.9 million barrels per day in 2010. Canadians consumed only about 1.8 million barrels per day that year. So, how is it possible that 43 percent of their needs had to be imported? (The number was 65 percent for the provinces from Ontario eastward.) The answer is straightforward once you get a glimpse of the North American oil pipeline system. Notice that the one lone pipeline going from Montreal to Sarnia is flowing away from eastern Canada. (Click on the map to see a larger version.)

Most of Canada's oil wealth is found in the western part of the country. And, nearly all of the pipelines run north/south, exporting much of that oil into the United States. When one asks why this is so, the answer given is that this is what has proven to be most economical. Western Canada exports its oil to the United States. Eastern Canada imports most of its oil from abroad. That works fine until there is a disruption in supply. This year, in particular, ought to give Canadians cause for worry given all the social unrest in the Middle East and the civil war in Libya which resulted in substantial output losses.

When Canada's oil riches are combined with its abundance of natural gas--it exports half its production to the United States--and its large deposits of uranium and coal, the country ought to be energy self-sufficient. So, why haven't Canadians pursued energy independence? One member of the Canadian parliament thought he had an answer all the way back in 1972. Don't worry too much if you can't follow his discussion of oil company takeovers at the time. His conclusion, however, is quite clear: The Canadian oil industry is largely foreign-owned and serves the needs of its corporate masters and not those of the Canadian people. Little has changed since then.

The current Canadian government seems nothing more than a subsidiary of the international oil industry which finds it more profitable to ship Canadian crude oil out of the country and add value to it through refining operations elsewhere. So complete is the control of the industry over the government that a witness before a parliamentary committee who broached the subject of Canadian energy independence was told to cease his testimony, and the hearing was immediately adjourned by the Conservative Party chairman who presided.

What might the advantages of building an east-west pipeline from the tar sands to eastern Canada be? Of course, there would be many Canadian jobs created by the building of the pipeline, and that would also benefit the government through increased tax revenues. Ports in the east might become oil export terminals instead of import terminals. Canada would likely build more domestic refinery capacity, both to supply its own needs and to export refined petroleum products. That would lead to yet more jobs for Canadians and yet more tax revenue for their provincial and federal governments. And, that would mean better financed public services for all Canadians.

Naturally, the large international oil companies that control most of the Canadian oil industry want to avoid the high taxes generally levied throughout Canada. Better to ship oil to the lightly taxed United States, refine it there, and sell it back to the Canadians or whoever offers the highest bid.

There is another way in which the international oil companies have thwarted Canadian energy independence. The North American Free Trade Agreement (NAFTA) prevents Canada from reserving more its oil production to itself in the event of an emergency. Canada is obliged to maintain the same ratio of exports to total production that prevails in any preceding 36-month period. No sudden cessation or reduction is allowed unless it is due to a decline in total production, something not in prospect anytime soon in Canada. (It's worth noting that Mexico, a major oil exporter to the United States and a signatory to NAFTA, refused to sign such an agreement.)

NAFTA also prohibits Canada from charging a lower price to domestic oil consumers than to those purchasing exports. It's common practice for countries that are self-sufficient in oil to give domestic oil consumers a discount from the world price, in essence, to control domestic prices. Back in March of this year when vaulting oil prices pushed up the cost of refined products such as gasoline, residents in some oil-rich countries hardly noticed. Kuwaitis were paying 81 cents per gallon for gasoline. Saudis paid 45 cents. And, Venezuelans were paying just 6 cents.

Since Canada imports so much of its oil, it has little choice but to accept the world price. (It could subsidize oil using funds from elsewhere in the economy, but that would be extremely costly.) Whether it is good policy to provide low-cost domestic fuel is questionable since such a policy tends to encourage profligate use. Some exporters that could easily afford low domestic oil prices choose just the opposite course. Norway, the world's eighth largest oil exporter, was charging $9.27 a gallon (including taxes) for gasoline in the same March survey mentioned above. The point remains, however; Canada currently has no choice. Its energy sovereignty has been severely restricted.

Of course, Canada could withdraw from NAFTA by giving six months' notice. This might prove painful as the United States would likely retaliate in several other areas of trade and reciprocal relations. In the alternative, the Canadian government could reopen the NAFTA agreement and alter the section on petroleum to allow it to route some or all of its increasing tar sands production eastward within Canada. But, don't look for this to happen anytime soon.

The impression I get is that most Canadians do not even know that their government has essentially given away their energy sovereignty to the United States through NAFTA. The onesidedness of the agreement was made plain by the U.S. rejection of Chinese National Offshore Oil Corporation's attempt to buy U.S.-based Unocal. There was overwhelming political opposition to this acquisition--even though Unocal had relatively small domestic operations--because the takeover represented an attack on American energy security. Any foreign power seeking access to American oil is probably facing an unwinnable fight. Canadians, however, are basically helpless in the face of American demands for Canadian oil. No wonder American politicians speak of Canada's resources as if they are located inside the United States.

Many who are protesting the Keystone XL pipeline--the formal name for a project to extend existing pipelines that would increase the export capacity of the tar sands to the United States--don't want it because they believe tar sands production produces significantly higher greenhouse gas emissions versus conventional oil production. Some also object to the wholesale destruction of forests, cleared to make way for tar sands mining operations which then cause air and water pollution.

To this list of concerns, Canadians should add a query about why their patrimony of oil resources is being shipped to strangers when so many Canadians remain dangerously exposed to disruptions in oil imports transported from faraway sheikdoms. There is no good reason why Canadians must bear such a risk. But there is one bad reason: Canadians have lost control of their energy resources, and those resources have long ceased to be managed for their benefit.

Which begs the question: Would Canadians want that control back if they understood their predicament correctly?

___________________________________________________________________________________

RELATED UPDATE October 21, 2012: Canadians could free themselves from oil imports, but will they?

Sunday, November 20, 2011

Emperor Vespasian has a solution for unemployment

One would think that given the scope of such a project and the other projects built under his reign that Vespasian would have welcomed suggestions for increasing the efficiency of construction practices. But he didn't. Instead, as historian Michael Grant reports in The World of Rome:

[W]hen Vespasian was offered a labor-saving machine for transporting heavy columns, he was said to have declined with the words: "I must always ensure that the working classes earn enough money to buy themselves food."

Of course, Vespasian had to contend with a slave workforce which he needed to keep busy and free working-class Romans who needed to be fed. We don't allow slavery (unless you count the sweatshops of the world as its successor); but the idle workforce, especially of the unskilled, continues to expand.

I was reminded of Vespasian when Charlie Hall, perhaps the best-known energy researcher you've never heard of, commented at a recent conference that we have built a society where fossil fuels have consistently displaced labor. This has had the unfortunate result that those whose primary aptitude is with their hands are finding less and less work.

Of course, much of the manual work which used to be performed in the United States is now done in the Far East, particularly China. And, the kind of work that most factory workers do there might very well be considered drudgery by many people. Hall's point, however, was two-fold. First, impending declines in available energy to society will likely force such work closer to the markets it serves. This is because rising transportation costs will diminish the advantage of worldwide manufacturing webs in favor of regional and local ones. Second, manual labor often requires skills that we in the United States do not teach as widely as we used to. We aren't ready to make the things we once made. And, all of this remains true even as the ranks of the unemployed swell and energy costs continue to climb.

Certainly, Vespasian's attitude would have prevented the immense advances in productivity of the modern age. But since those advances are largely premised on the growing availability of cheap energy inputs, we may need to re-examine our attitude as those energy inputs become constrained and thus are no longer cheap.

Moreover, continued policies that lessen opportunities for manual labor will, of necessity, doom an entire group of people to the unemployment rolls just because their intelligence shows through in what they make with their hands rather than what they say or write.

I am not here romanticizing backbreaking labor. The one place that mechanization has failed to progress very much in the last few decades is the picking of fruit. Researchers had been looking for ways to harvest fruit mechanically. But an onslaught of cheap immigrant labor into the United States from the 1980s onward pushed real wages down for farm labor so far that mechanized fruit picking did not seem worth the effort. Even in the exploitative world of farm labor the laws of supply and demand apply. An avalanche of new workers depressed wages and doomed the mechanization effort.

We may be facing something similar in the next decade. The financial turmoil of Europe is but the latest chapter in what I believe is an unfolding depression that will take many years to resolve itself. It is worth remembering that as late as 1931, no one alive back then thought they were in a depression, let alone what would come to be called the Great Depression. Back then, of course, governments engaged in very little of what we would call stimulus, and central banks did not regard it as their purview to save the economy and provide full employment. We have bought some time with countercyclical measures from both institutions. But now the effects are running out, and we must face the consequences of too much debt and not enough cheap energy.

During the Great Depression President Franklin Roosevelt proposed and implemented huge government works programs, the results of which can still be seen today in forests that were replanted and dams that were built. Such programs put people to work on useful public projects largely with their hands. Advances in productivity are useful, but useful work is more important to the human psyche and thus to social stability.

Jay Hanson, one of the first to publicize approaching resource limits through his dieoff.com site, was recently quoted as saying that the most important issue to face society in the coming era of limits is what to do with all the young men. No one needs to be reminded what can happen when this subgroup of society sees no useful role for itself. One way in which many societies solve this problem is to send the young men to war. And, certainly, the United States and others might try this as a way to harness the restless mass of unemployed young people. Of course, the stimulative effect of war on the economy is well-known. (This is assuming your country is not being destroyed by the war.)

In the coming era of limits we will need to rely less on fossil fuels and more on each other. "Idle hands are the devil's playground" will become more than a trite aphorism if we do not see that the future will require us to find more work for idle hands. The work is there to do, to restore our environment, to teach the young, to repair our crumbling infrastructure and to rework it for a lower energy future.

Those in the skilled trades are available for these tasks. Those who are unskilled will need to be brought into the workforce, paid decent wages and given reasonable working conditions. We can argue all we want about economic theory and market-determined wage rates for such people. But the alternative to providing decent wages and conditions for the least skilled among us is an army of unemployed, dissatisfied and potentially disruptive people whose potential contribution to society will be wasted because of a slavish devotion to free-market ideology.

The fantasy that machines will more and more dominate our lives will only come true if there is the energy to fuel them. Absent that, we will be forced to rely increasingly on our hands and our feet to do the daily work of living. Vespasian understood that hands and feet need something to do that produces a living. The sooner we see that, the better.

Sunday, November 13, 2011

Sunday, November 06, 2011

Time to worry: World oil production finishes six years of no growth

As oil prices rose ever higher in the last decade, the optimists kept predicting rising production capacity and plummeting prices. Looks like they got it wrong. Read more.

Sunday, October 30, 2011

Not so much: Shale gas shows its limitations

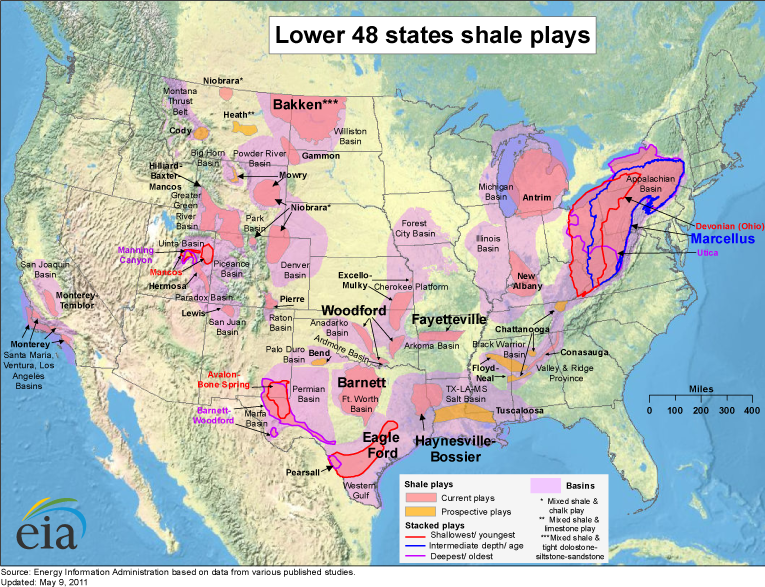

Though the ads will probably not be withdrawn or recut, the emerging facts run counter to the gleeful tone of this television commercial produced by America's Natural Gas Alliance, a consortium of shale gas drillers. (For some more samples from other advertisers, click here, here and here.) First, it has become increasingly apparent from actual well data that shale gas is not being harvested according to the much-touted "manufacturing model." This model assumes that shale deposits are basically uniform, or at least uniform enough that a driller could sink a well virtually anywhere in a shale gas deposit and have an economical well blasting out methane.

Independent petroleum geologist Art Berman and his colleague Lynn Pittinger, who studied the actual data, have shown that the manufacturing model is a myth, to wit: "The contraction of extensive geographic play regions into relatively small core areas greatly reduces the commercially recoverable reserves of the plays that we have studied." In short, you can't just drill anywhere. Drillers thought the huge plays highlighted in pink on the map below would yield profitable shale gas everywhere. It turns out that there are sweet spots, and then there are spots that are not sweet at all. And, the sweet spots are turning out to be quite small compared to the size of the deposits.

Berman and Pittinger also point out that initial high flow rates give out within a couple of years, putting drillers on a treadmill merely to replace this declining production and implying geometric increases in the number of wells they must drill to grow production consistently. What's more, the two authors question claims of decades-long flows, albeit at very low rates, from individual wells. The history of shale gas wells to date suggests that this is unlikely at best, and almost certainly uneconomical.

The second shoe to drop was a piece in The New York Times entitled "Insiders Sound an Alarm Amid a Natural Gas Rush" which cited internal memos and emails from industry and government officials admitting that estimates of the available gas from shale are overblown.

The third piece of damning news came from a recent U.S. Geological Survey (USGS) assessment of the Marcellus Shale natural gas deposits, by far the largest of their kind in the United States spanning vast areas of New York, Pennsylvania, and West Virginia as well as sections of Ohio, Kentucky and Tennessee. Previously, the U.S. Energy Information Administration, the statistical arm of the U.S. Department of Energy, had estimated that the Marcellus Shale contained 410 trillion cubic feet of so-called "technically recoverable shale gas resources." (This says nothing about whether such resources can be economically recovered. See the discussion of natural gas prices below.) The USGS report put the technically recoverable amount at 84 trillion cubic feet, an 80 percent reduction. For reference, the United States consumed about 24 trillion cubic feet of natural gas in 2010.

The often repeated claim that the United States has 100 years of natural gas at current rates of consumption is based to a considerable degree on the 410 trillion cubic feet which the Marcellus Shale supposedly added to U.S. resources. But, don't expect the shale gas drillers to stop advertising the 100 year claim anytime soon.

The fourth piece of news came not from industry insiders or studies of Mother Nature herself, but from state government. As I wrote earlier this year, new regulations could significantly dampen shale gas production. The newly released regulations in New York state do just that and to a degree that even I didn't think possible. Buffers are now required around water resources and have cut down the area available for drilling within existing shale gas leases by 40 and 60 percent. In addition, some municipalities are using their land use regulatory powers to make it all but impossible to drill in their jurisdictions.

As a result drillers are furious, so furious that some are thinking of abandoning their leases to concentrate on drilling in states with more lax regulations. New York may bid them a fond farewell since the legacy costs of cleaning up aquifers and drinking water could in the long run far outweigh the temporary economic gains from natural gas production.

Finally, there is always the question of price. A drilling foreman I know told me not too long ago that we might have quite a bit of natural gas available above $10 per thousand cubic feet, but not very much below $4. Price matters because the huge amount of natural gas promised by the industry would require the exploitation of deposits that are expensive to develop and therefore require prices much higher than today's.

I expect there to be a fifth, sixth and seventh piece of news and so on, detailing new limits on the rate of shale gas extraction. True, the explosive growth of shale gas production certainly caught many energy analysts by surprise. The received wisdom up until recently was that conventional gas production would decline, and the United States would increasingly rely on imports. But, I think the public and policymakers, who are being propagandized daily by the industry, may be in for yet another surprise.

Abundant natural gas? Sort of, but only if the price is right. Cheap natural gas for the long run? Not so much.

Sunday, October 23, 2011

Don't gamble with the grocery money

It sounds simple enough. But the real trick is to figure out whether you are gambling with the grocery money. I began thinking about all this as I was seated next to a woman retiree on a train ride during a recent trip. We got to talking about the Occupy Wall Street protest, and we went on from there to talk about the stock market and retirement savings. I suggested to her that the retirement savings of the entire middle class of America are at grave risk. I explained that the seeds of that risk were sown back in the early 1980s when a then little-known provision of the tax code labeled 401k--which was designed to encourage supplementary retirement savings--was used to transfer all the risk of pensions from companies to employees.

Before the 401k craze (403b for nonprofits) companies with pension plans generally guaranteed a specific benefit, i.e., an amount per month that would be paid to retirees for life based on years of service, pay level and sometimes other factors. It was up to the company to figure out how to make that happen with money set aside usually through both employer and employee contributions. The company often hired outside money managers to invest the money based on the projected needs of retirees. Such plans are usually referred to as defined benefit plans, and they were the norm before the 401k. Now, they are rare.

The result has been that every person with a 401k has had to become an amateur investor. And, all seemed well from the early 1980s onward when such plans first came into widespread use. The world had just embarked on what would turn out to be the biggest bull market in stocks ever seen. As John Kenneth Galbraith once said, "Financial genius is a rising stock market." It became common wisdom that everyone should own "stocks for the long run." We were told we were in a "new era" of unprecedented technological progress. We were also told that monetary authorities had now mastered the business cycle through their clever manipulation of interest rates and other levers of finance.

(It is puzzling why anyone would continue to assign omniscience and omnipotence to central banks and governments after the Bear Stearns collapse, the 2008 crash, phase one of the European debt crisis last year, and now phase two of the European debt crisis. If central banks and governments are so powerful and all-knowing, shouldn't they have been able to prevent these serial financial implosions?)

Back to the poor woman sitting next to me on the train. I suggested that faith in the narrative described above was borne of a highly unusual period of history, and that one has only to go back to The Great Depression to find that it is possible for the stock market to decline 80 percent and not recover to its old highs for two and half decades. (I forgot to mention that today Japan's stock market is down more than 75 percent from the high it reached in 1989!) I suggested that the current system of retirement finance was largely concocted to relieve corporations and other institutions of their retirement obligations to employees and to enrich Wall Street. Wall Street, after all, gets its fees whether the client makes money or not.

I proffered that the game was a dangerous one for all but the largest players. Why? Three reasons: First, those players have access to information, connections and great gobs of capital that can move markets, and they are perfectly capable of making money when markets go down as well as up. Second, they have so much money that even severe losses will not prevent them from buying groceries and paying their mortgages and utility bills. Third, the government will step in to prevent them from going bust if it believes this means preventing a systemwide financial meltdown.

Were average people like her really in a position to compete with that? I asked. I thought to myself that this woman and so many like her are not playing with money they can afford to lose. They are gambling with the grocery money and they don't even know it! And, that's because they've been sold the idea that they are investing which sounds a lot nicer than gambling. But it amounts to the same thing.

Of course, if everyone took my advice tomorrow, the stock market would collapse. But my argument is that we should have never have gotten to this point. We should never have abandoned a system that makes retirees essentially indifferent to the level of the stock market. But because of the move to 401ks, many are now risking losing their grocery money and do not seem to know it.

Perhaps my fears are unfounded. But as I look at the amount of gray hair in the crowds at various Occupy Wall Street events, I wonder if a lot of damage hasn't already been done. The last 10 years have netted the average investor essentially nothing. And, the most recent market swoon has once again tested hopes that the casino profits in the market can continue.

With the Europeans outdoing the Keystone Cops as they slide toward an ineluctable default in Greece and a possible worldwide contagion; with a worldwide economic slowdown and possibly a recession already underway; with rumors arising nearly every day that one bank or another may soon go down; and with a severe property bust already evident in China, I fear there is worse to come.

Sunday, October 16, 2011

Can Margaret Atwood's environmental message reach a broad public?

All of that has been done, of course. And, it would be unfair to say that it has had no effect. There is now a markedly larger group of people in the world who are conversant about all the major climate, resource and environmental problems we face. There are even many more politicians and policymakers who've been educated in this way. But instead of the swift, decisive action one might expect to address these onrushing catastrophes-in-the-making, the response--when there has been any at all--has been rather tepid.

One reason is that politicians by their very nature are inclined to do only what the public will let them do. (Naturally, they'll often do things which are not in the interest of the broad public if that public is unaware of what the politicians are doing.) But when it comes to complex, knotty issues such as climate change and peak oil, there is no wealthy constituency which can arrange midnight deals out of view of public scrutiny. That means there must be public pressure intense enough to motivate politicians to act. It has to be so intense that they think they might lose an election over such issues.

Perhaps there is another avenue of public persuasion that is up to this task. We need a compelling narrative, I often hear. So true. But what makes a narrative compelling? Certainly, it must be simple enough to be understood by a broad group of people. Check. And, it must play on values that people already hold dear. Check. Finally, it must be in a form that is readily acceptable and easily obtained by the target audience. Check.

Now, the problem, of course, in that a compelling narrative about our climate, resource and environmental challenges would be hard to make simple. The whole point would be to make it clear that these are complex problems with no easy solutions. And, the whole point would be make it clear that these problems arise from the totality of the way we live, making it difficult to appeal to existing values. And, the whole point would be to startle people into a mode of awareness that goes beyond their current way of seeing.

In The Year of the Flood Margaret Atwood attempts such a narrative in an almost fairytale fashion. The clever thing about the novel is that it appears to be a typical post-apocalyptic story, taking us to an indeterminate locale in the future in which two young female characters find themselves caught in the great "waterless" flood, a plague that is devastating the population. But we quickly move back in time. We follow these characters as they work and wander in this pre-plague futuristic world, one that seems dysfunctional and violent in ways that are familiar to us today. So far, it's pretty standard science fiction stuff.

But then the two women end up joining the friendly Gardeners' cult whose members are so gentle and wise that one is lulled into thinking that Fred Rogers might suddenly appear at the edge of their rooftop garden, eager to take his television viewers on a tour. The impression that some of the Gardeners might have been descended from the Amish seems well-founded. How quaint they are in this world of advanced genetic technology.

Gradually readers are pulled into a sinister world controlled by private security firms which now run the police force and the prisons and which also guard corporation employees who live in isolated compounds. The corporations have become ascendant and their technological vision of the world knows no constraints. This is because a badly run authoritarian, corporation-dominated state has replaced all other civil authority. Everyone must have a state-sanctioned identity, and deviations from the corporate line, i.e., all technology is good for us and corporate control brings prosperity and health, can mean loss of a job and even prison time.

The science fiction fantasy elements of the story actually comport well with the expectations of modern readers. So, in this respect Atwood has managed to overcome possible resistance to her narrative. The religious views of the Gardeners' cult are summarized in occasional addresses by the leader of the group, Adam One. (Only in a society completely hooked on genetically engineered food would people who grow food in a garden be considered a cult.) The religious discussion makes it possible in some ways to bypass the modern industrial mind and reinitiate contact with the natural world using religious metaphors from agriculture and nature. And, this makes it possible to explore values that readers might harbor apart from the industrial corporate world.

For all these reasons I believe Atwood has produced a master work of environmental awareness. This novel, which appears to be merely the fantasy of a talented Canadian author is, in fact, meticulously researched. Its references to genetic engineering are not merely fanciful but anchored in actual ongoing scientific work. The story exaggerates for effect, of course. But its dissection of the food system (one main character works briefly for a fast food chain called SecretBurgers) is clearly drawn from a keen understanding of our current system. The privatization of every public function seems overblown, but suggests the logical extreme of our current trajectory.

A well-designed narrative enters the mind at both the conscious and unconscious levels. I am reminded of the film Avatar which, though a piece of science fiction, is essentially a story about the displacement of indigenous people by a ruthless corporation to enable the mining of a valuable mineral. Right-wing pundits decried the film as an attack on American foreign policy which they said has historically helped to spread democracy and prosperity. No matter. Moviegoers liked the film as much in Alabama and Mississippi as they did in California and New York. Whether the film changed mindsets is unknowable. But it had no trouble gaining acceptance.

Atwood's novel is not a movie, not yet anyway. And, so even its well-founded success will still result in only limited influence. After all, one must buy it. For most people that will cost quite a bit more than a movie ticket. And, then one must devote many hours to reading its 400 plus pages. But The Year of the Flood does offer an interesting blueprint for the successful environmental/resource/climate-change story. And, for that reason it would behoove all those who are searching for ways to reach the broader public about these important issues to read this remarkable work.

Sunday, October 09, 2011

Destroying dreams the peak oil way

Certainly, a persistent, irreversible decline in world oil production would reshape nearly every facet of our lives. I like to think that we don't need to give up on our dreams, just choose different ones that are achievable in the challenging environment we are likely to encounter as the coming decades unfold. And, I like to think that those dreams can be as much, if not more, satisfying than our current ones.

That's cold comfort to those whose entire education is designed to prepare them for exceedingly narrow occupational niches, niches which they've been told will bring them wealth and security. It is an unfortunate truth that in a world climbing down from unsustainable complexity (fostered by previously cheap energy supplies), many of those niches will disappear.

I've come to understand that most people cannot imagine a future that is different from the recent past--and by that I mean the past few decades. And, this tells me that until the past few decades are a fading memory, most people will find imagining an entirely different future an insuperable task. Even as conditions worsen, they will assume that if governments will just take the right steps, then the world will return to its former path of exponential growth and unlimited opportunity. They will assume this because opposition parties will tell them so just to get elected.

As the world's financial markets gyrate wildly, I find myself in conversations that touch on investing with both family and friends. With family members I am much more forthright about how I perceive the risks we face. I know that my family members will forgive my brash interventions into their lives and that, in any case, they are all strong enough to ignore me and think for themselves. But with friends I am reluctant to speak about such matters and only discuss them when others introduce the topic. If I am asked for my opinion, I currently urge extreme caution. (Full disclosure: I exercise exactly two levels of care in investing: caution and extreme caution.)

The response more often than not is that, while stocks are down, they always go back up, and so naturally, it's not smart to sell your stocks when they're down. This sounds suspiciously like the person who is losing at roulette and sticks around in hopes of winning her money back. It's hard to counter people's recent experience, i.e., the last three decades which delivered the greatest bull market of all time in stocks. And, it's even harder to convince them that history is replete with examples of stocks falling to a rather small fraction of their highs under conditions very similar to those which prevail today. Japan--whose market is down more than 75 percent since 1989--comes to mind.

But I now realize that there is a dynamic here similar to that which I experience with college students. Middle-aged people with retirement savings have dreams, too. And, my suggestion to exercise extreme caution, i.e., get out of the stock market and into cash, is tantamount to telling them that they cannot have their dreams. So many who have saved for retirement by investing in the casino called the stock market believe that said stock market will provide the money to pay for dreams their regular salaries could never have financed.

This dynamic, unfortunately, is yet another roadblock hindering people from taking steps to salvage what future they can. Would-be destroyers of dreams, beware! You will have the ear of fewer and fewer people over time as many tune you out in order to preserve the image of the future they have in mind.

Of course, I could be wrong in my views and miss out on participating in and getting rich from a great economic boom ahead that will inevitably come after our leaders clear away the few small hindrances that remain. But then I'm not sure I really want what that path has to offer, even if it turns out to be available. In that sense, I'm covered for both positive and negative outcomes since our present arrangements, economic, social, political and occupational, seem less and less alluring with each passing day. Maybe that's the key to giving up on the dreams we've been taught to dream and dreaming something altogether new.

Sunday, October 02, 2011

Crisscrossing the Rubicon of peak oil

But even as some of these symptoms begin to manifest themselves, the public remains ignorant that stringency in oil supplies lies at the heart of them (though peak oil is admittedly part of a complex web of problems related to our broader energy and resource use). Why is this so?

From the long view the level of oil production on a graph in this decade may well look like a peak. But from closer in, as we experience it day to day, month to month, and year to year, production may seem to be on a long, bumpy plateau. Even though one of the world's major sources of energy information, the International Energy Agency, admits that conventional crude oil probably peaked in 2006, the public and most policymakers remain ignorant of this sign that liquid fuels will have a hard time keeping up with demand.

It is true that other liquids--natural gas liquids, biofuels and unconventional oil derivatives--have allowed total liquid fuels production to eek out at new all-time high this year. But robust demand once again drove the price for Brent crude above $100 where it remains as of this writing. This seems to have had the effect of dampening economic activity and so prices and production have actually fallen from their highest levels as demand has waned. We know that oil price spikes have been associated with 10 of the last 11 economic recessions (PDF); there is reason to believe that we are headed into number 12.

It is this pattern which prevents a clear signal to people, policymakers and markets about our predicament. We seemed to be crossing the Rubicon of peak oil in 2008 as prices rose to $147 a barrel only to cross back during the subsequent two and a half years leading to a new nominal peak in production in January this year. In between the price of oil plummeted to around $35 a barrel before rebounding above $100.

This phenomenon has now been described for us by the former editor of Petroleum Review, Chris Skrebowski, in his piece "A Brief Economic Explanation of Peak Oil." Skrebowski believes there is a sort of speed limit that oil prices are imposing on the economy, and it begins roughly when oil trades above $90 a barrel though the number may be higher for high-growth countries such as China, perhaps up to $110. If prices stay in this area for long, it appears to signal that a recession is not far away.

From the public's point of view, oil prices this high have become a "normal" part of life. And, if Skrebowski's analysis proves correct, there will be no dramatic price spikes above, say, $200 a barrel that stick, something that might definitively signal the beginning of a long-term oil crisis in the public's mind. Instead, there will be repeated attempts to revive economic activity through fiscal and monetary stimulus which will ultimately fail to gain traction as oil prices shoot up once again, dampen economic activity and lead to recession after recession. During each recession oil prices will drop making the peak oil problem seem to disappear.

It's certainly true that significant increases in world production of liquid fuels would end this cycle. But as Skrebowski points out, "If adaptive responses were fast enough and large enough, oil prices might be broadly stable. They clearly are not." By "adaptive responses" he means in part those increases in oil production and the production of substitutes. But, the unstable economic climate we are now facing is making long-term planning and investment in both the oil industry and the alternative energy industries difficult.

What Skrebowski offers is a sound rejoinder to those economists who say that peak oil theorists don't take into account economic factors--factors which those economists say will solve the problem of peak oil whenever it arrives by destroying demand and making substitutes profitable. For now, however, we can see that the economic factors are not really solving the problem of peak oil, but possibly feeding it. That's not something most economists will be able to hear. And, it describes a pattern that will likely only confuse the public and policymakers even though Skrebowski has explained it in terms that any thoughtful person can understand--if only they want to.

Sunday, September 25, 2011

Ignoring Daniel Yergin

But back in the rarified realm of the energy-obsessed we find two responses posted under the headline: "Daniel Yergin - Oil Company Whore." I was expecting some red meat. But the worst that either of the writers of these responses could muster is that Yergin is a "Pulitzer Prize-winning historian" and not particularly well-qualified to assess future oil supplies. In the comments under these pieces (all rebuttals), one commenter calls Yergin "the Alan Greenspan of the oil industry--the guy everyone thinks is a genius...until he is proved disastrously wrong." It's an unflattering comparison, but only to those who understand both who Alan Greenspan is and the complex reasoning behind the charge that he is the architect of our current economic troubles.

In truth, upon reading Yergin's latest missive to the world's policy elite, I found myself utterly bored. Could this man ever say something that would upset anyone other than a small group of activists who are extremely worried about oil supplies peaking before the end of this decade? I doubt it. He is paid to soothe, and these days so soothing is his writing that it should be placed next to the Sominex on the drugstore shelf.

Certainly, those concerned about how policymakers think about our energy future will feel compelled to respond to this craftily written piece and to Yergin's newest book--a continuation of his famous history of oil, The Prize, but with a broader focus. Even if the respondents succeed at denting the minds of policymakers, what can they achieve? Wherever the peak oil movement plays at the inside game, it will be at a disadvantage. It is far easier to throw sand in the gears of a representative democracy than it is to get anything done. And, it is far more difficult to get people to prepare for a challenging future of energy stringency than it is to convince them that the future of energy should be entrusted to upbeat experts in suits.

I write all of this to lay out briefly the arena in which this battle of ideas is joined. It is an arena chosen by Daniel Yergin in which he has many preponderant advantages. He may be a Pulitzer Prize-winning historian with no formal geological training, but he's also the head honcho of the world's most recognized brand in energy advice, Cambridge Energy Research Associates (now absorbed by IHS). He is a frequent face at Congressional hearings and a man who hobnobs with kings and prime ministers the whole world wide. It is hard to convince anyone at the top levels that he doesn't know what he's talking about, especially when the world's major newspapers and broadcast venues give him access usually reserved for high government officials.

No matter how well-reasoned one's arguments are, as a tactical matter, a head-to-head confrontation in the media with Yergin will be a draw at best, but more likely a loss since reason is not what moves crowds. I agree that the fact that Yergin must now address peak oil explicitly and at length shows that he is actually on the defensive. Before, say, 2005 he wouldn't have bothered even to mention it. This shows some progress, but not among those who matter most.

There is a vast audience of people out there who, as I said, have never heard of Daniel Yergin, and who have never even heard the words "peak oil." The elected officials who guide our policy will do little to address peak oil and related issues until voters communicate that these are top priorities that will affect elections. Beyond this there is the issue of encouraging personal preparedness, something that is in large part outside the scope of government policy.

I was involved in discussions about how to respond to Yergin's long tirade against the peak oil movement. Should the response be point-by-point, or should we just make our case the way we want to? Whether it's the inside game or a more extensive public education strategy, the answer should be obvious. We should largely ignore Daniel Yergin and find better ways to convey not just the facts about energy, but also model an appropriate emotional counterpoint that will penetrate hearts and minds in ways that Yergin's sleep-inducing message never will.

Sunday, September 18, 2011

Are we all rogue traders now?

My question is quite simple. If these traders had made billions for their institutions instead of losing them, would they have been labeled "rogue" and handed over to the authorities? I ask this question because it seems to me that what is being punished is not excessive risk-taking, but rather excessive risk-taking that loses money. Almost nobody labels risk-taking "excessive" if it results in a win. Then it is called "brilliant" or "gutsy" or "a stroke of genius." And, people who take such risks get large bonuses and are promoted.

In 2008 when nearly everything went sour for traders in the world's largest banks, the losses were explained (by the banks and their strategists) as the product of an unbelievably rare confluence of events. When one trader loses a large amount of money, he or she can be labeled "rogue" or, at least, suffer a quick dismissal. But when nearly all traders at a bank have their heads handed to them at the same time, it's not called excessive risk-taking, but rather a fluke.

What is not apparent in all of this is that banks and their risk analysts refuse to acknowledge that they face hidden risks which they cannot quantify because they cannot know about them. Risk models are one thing; the real world another. To my mind that makes all but the most conservative bankers "rogue" traders.

What motivates the non-conservative ones is the certain knowledge that the government will backstop them. As it turns out, the banking system historically has never made money and, in fact, lost money in the long run. The one thing it has done quite well is provide bonuses for its traders and managers--which they don't have to give back when their institutions go bust from their bad trades and loans even as the government bails them out. (To hear Nassim Nicholas Taleb, author of The Black Swan, explain this, see his congressional testimony: Part 1 and Part 2.)

The current maelstrom in the financial world, however, is not a discrete event. Our attitude in general about risk, especially low-probability, hidden risk, is similar to that of the man who sleeps on the railroad tracks but does not know about the existence of trains. Much of the time he can sleep there undisturbed. But he need only be wrong once in his timing to suffer catastrophe.

We have become a society reliant on expert forecasts. In the field of energy, many forecasters make fancy livings pretending to know the future supply and price of various energy sources, especially fossil fuels, projecting sometimes decades into the future. Not wanting to rely on outsiders, governments routinely hire their own experts to make energy forecasts for them. And, policymakers and managers everywhere in society make fateful decisions based on those forecasts without knowing how uncertain they are.

Given how central energy is to the functioning of society, nearly all of us have become in some ways like rogue traders, basing our lives and plans on comforting models that contain hidden risks and may have little resemblance to the future we will live in. In that sense, UBS's rogue trader and, in fact, the entire world of financial traders, may be a mirror for society in general, one that we would do well to examine. We might see that energy and so many other systems rely on forecasts with hidden risks for which we have built in little or no margin of safety. Unfortunately, there will be no central bank of energy or any other essential resource to bail us out as those risks make themselves evident.

Sunday, September 11, 2011

A guide for the perplexed energy policymaker

If you are an energy policymaker (or layperson interested in energy) and you are NOT perplexed by the last decade, read no further. You have little to gain from what I write below. However, if you are a perplexed energy policymaker (or perplexed layperson interested in energy), please continue and learn why poor quality data, lack of transparency, broad uncertainty and flawed thinking about risk have made it difficult for many experts and the public alike to think sensibly about our energy future.

Several often unexamined assumptions made by many of those engaged in energy policy and analysis obscure how they arrive at their conclusions. Those assumptions include the following:

- Fossil fuel resources are so vast that we need not concern ourselves that their supply will start to decline anytime soon.

- Technology will always allow us to extract these increasingly difficult-to-get fossil fuel resources in the quantities we need at the time that we need them at prices we like. Prices, it is believed, will govern this process in a completely benign way, that is, high and volatile fossil fuel prices won't destabilize the complex systems of modern society in a way that might impair them in the long term.

- Substitutes for fossil fuels will be introduced gradually in accordance with market signals and will grow commensurate with our need for them. A smooth transition away from fossil fuels will succeed incrementally over many decades.

- The data on fossil fuel supplies is either sufficiently robust to reassure us of benign outcomes or the data do not matter since reserves of fossil fuels and the substitutes for them will expand in accordance with market signals thereby vindicating optimistic forecasts for future energy supplies.

Whether such assumptions form the basis for sound energy policy is the subject of this piece.

Poor quality data, lack of transparency

The first thing a perplexed energy policymaker must grapple with is the fact that 86 percent of the energy used by human societies currently comes from fossil fuels. This overwhelming dependence on finite supplies of stored fossil carbon in liquid, gaseous and solid form suggests vulnerability all by itself. But perhaps more worrying is the lack of transparency concerning known underground inventories of these fuels.

For petroleum many analysts rely on the BP Statistical Review of World Energy which also includes information on natural gas, coal, nuclear energy, hydroelectricity and other renewable energy. The data provided in the review is simply that reported by various governments or from published sources. The reliability of that data, however, cannot be assured. One example that raises suspicion is the curious jump in reported reserves among OPEC countries in the mid-1980s. At the time OPEC changed its rules to take into account the size of reserves in assigning a production quota for each country. The bigger the reserves, the larger the production quota. So, this curious jump can be explained by the equivalent of grade inflation in the oilfields of OPEC. Skeptical observers have dubbed these phantom additions "political reserves" and usually subtracted all or some from official tallies of world totals.

Further adding to skepticism about the reported numbers are long, unchanging series which indicate that some reported reserve numbers almost surely do not reflect changes on the ground in exploration and depletion. The United Arab Emirates has reported oil reserves of 97.8 billion barrels for the past 15 years. Kuwait reported 96.5 billion barrels in reserves from 1991 to 2002. From 2004 through 2010, it reported 101.5 billion barrels every year. Saudi Arabia reported reserves within a narrow range of 260.1 to 264.5 billion barrels from 1989 through 2010. At least those numbers shifted slightly each year.

The competition within OPEC continues to this day as Iran attempts to eclipse Iraq's newly updated reserve estimate. Are we seeing new "political reserves" or something based on actual exploration? Certainly, many analysts will offer explanations for these reserve numbers. But there is no way to tell for sure whether their explanations make sense since OPEC nations and many other countries do not submit to independent audits of petroleum reserves. So far, energy planners have simply had to take the word of most petroleum producing countries about their oil reserves.

At least the major publicly traded oil companies must meet a higher standard, right? Not exactly. First, it doesn't really matter that much since 80 percent of all reserves are held by government-controlled companies. Second, new U.S. Securities and Exchange Commission rules allow much more leeway for publicly held companies to report reserve numbers. Perhaps most relevant is the following from an SEC document finalizing the new rules:

We are clarifying that the required disclosure would be limited to a concise summary of the technology or technologies used to create the estimate. A company would not be required to disclose proprietary technologies, or a proprietary mix of technologies, at a level of specificity that would cause competitive harm. Rather, the disclosure may be more general.

The methods for grinding out reserve estimates can now remain secret. To outsiders reserve estimates will in many cases be coming from something which looks more and more like a black box.

Many of the same issues also apply to natural gas estimates since oil and gas are obtained using similar methods by the same industry. One reason for caution is the highly optimistic claims being made for natural gas supplies from shale deposits. The U.S. Energy Information Administration (EIA) has already decided that its methods may have overestimated U.S. production from shale gas wells by 10 percent in 2009, erasing much of the supposed 11 percent jump in domestic natural gas production.

As for reserves, there are many reasons to be skeptical about the reported reserves of shale gas including the failure to specify a price (since prices clearly influence what is economical to get out of the ground) and the booking of very low-return or just breakeven discoveries as a way to inflate reserves and promote a publicly traded company as an asset play. That the picture remains opaque should be cause for concern given the extravagant claims made for shale gas including its ability to displace oil and coal in the near to medium term.

The data for coal reserves are even more problematic since governments don't routinely do comprehensive surveys of coal deposits. The Energy Watch Group's paper entitled "Coal: Resources and Future Production" claims that Vietnam has not updated its stated coal reserves for 40 years. China has not done so since 1992 despite the fact that 20 percent of the country's reserves have presumably been produced since then. Even the venerable BP Statistical Review of World Energy has no historical data on reserves. And, the U.S. Energy Information Administration has reserve data starting only in 2008.

So poor is the data on coal that the National Academy of Sciences in a report issued in 2007 said it could not confirm claims that U.S. domestic coal supplies amounted to 250 years at current rates of consumption. The reported stated:

Present estimates of coal reserves are based upon methods that have not been reviewed or revised since their inception in 1974, and many of the input data were compiled in the early 1970s. Recent programs to assess reserves in limited areas using updated methods indicate that only a small fraction of previously estimated reserves are economically recoverable. Such findings emphasize the need for a reinvigorated coal reserve assessment program using modern methods and technologies to provide a sound basis for informed decision making.

The report suggested that supplies might amount to 100 years at current rates of consumption and urged a thorough survey. Of course, the 100-year figure does not take into account any increase in the rate of production over that period or any decline in production once the peak in the rate of production has passed.